Don’t Get Cheated! Questions to Ask Your Financial Adviser

26 September 2017

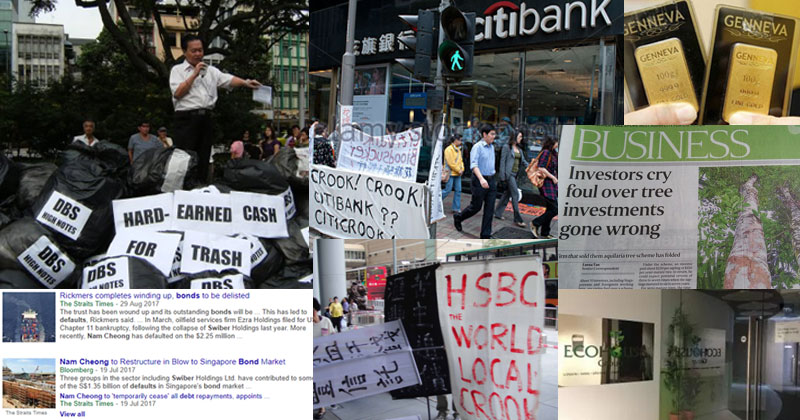

Do you remember reading all those sad stories about investors getting cheated out of their hard earned savings? The Straits Times and other local media have often reported on such cases – Singapore bond defaults, penny stock crash, various property investment busts, New Zealand property developer banktuptcy, various ponzi schemes, tree investments, sports betting investment, binary options, gold buyback scheme; the list just goes on.

It seems that it’s all been happening way too many times! But why is this so? Wouldn’t people wise up after a while and become more discerning of such claims? Or, is this the result of greed, where the urge to make money quickly results in both the investor and the salesman – or even the adviser – throwing caution to the wind?

However, there were also times where investors were just plain clueless. Our local regulator, the Monetary Authority of Singapore (MAS), has put in place some safeguards for investors. But if investors do not carry out proper due diligence and exercise common sense, then all the rules in the world will not save them.

The obligation of registered banks, brokers, investment and financial advisory firms to put their client’s interests ahead of their own is called fiduciary duty. Unfortunately, this obligation is not always practised, which results in poor advice and huge conflicts of interest. As such, for the most part, investors are left with Caveat Emptor – Latin for “Let the buyer beware”. Nonetheless, they can still arm themselves with this short checklist to ensure that they have engaged the right person – someone who will look after their interests.

MAS Checks

First, check with a few readily available online resources to see if the person you are dealing with is really who they claim to be. Make sure the firm you are dealing with is not on MAS’s investor alert webpage. The firms on that list are there for a simple reason – i.e. they sell unregulated investments, are not audited by the MAS or have been subject to investor complaints in the past.

The MAS’s list of financial institutions and relevant organisations webpage lists the firms which have been given a license by the Authority to deal in the specified regulated activities. Check to ensure that the company you are dealing with really has the proper license for what they are trying to advice or sell you.

Finally, each individual working for a regulated firm must also be licensed. Check this webpage to see if that person’s license is still valid and has not expired (the adviser representative is obligated to provide you with his/her representative number to let you verify his/her licensing status using the online MAS’ website).

Questions to Ask

Once you’ve established that your adviser is not part of a black-listed or fly-by-night company, you then have to ask the right questions to determine if he or she will act in your best interests. “How much money can I make?” is not the right question. Asking it will set you down the path to future despair. Instead, here are some good questions (and preferred answers in green) which you should be asking your adviser, broker or banker:

- What is your investment philosophy? (It should not include items from question 2 and 3, or bamboozly ideas like “proprietary quantitative mathematical algorithms”)

- Do you believe in stock picking, or market timing? (No)

- Do you believe you can consistently beat the market? (No)

- Are you a fiduciary, and would you put it in black and white? (Yes)

- Does anybody else ever pay you to advise me and, if so, do you earn more to recommend certain products or services? (No)

- Will you itemize all your fees and expenses in writing? (Yes)

- How often do you trade? (As little as possible, once or twice a year)

- Will you track my investment performance on a regular basis and tell me whether I am on track towards my goal? (Yes)

- Who manages your own money? (Myself. And I invest in the same assets I recommend to all clients)

- Can you tell me about your conflicts of interest, orally and in writing? (Yes)

- Can you tell me, orally and in writing the type of losses I could suffer by following your advice? (Yes)

You could mix and match whatever questions you wish and ask them of your adviser or banker. In fact, you could also go through the entire list and make your adviser sweat through the toughest job interview they would ever have to go through. Either way, simply talking through these questions would help you get to know what your adviser stands for before proceeding to part with your hard-earned money. You would then find yourself with a great adviser for life – someone who would not only have your interests at heart, but also be willing to guide you through all the perils and turmoil that come with managing money. It would be well worth the fee you pay him or her to receive that peace of mind, allowing you to focus on the things that really matter in life.

#

If you have found this article useful and would like to schedule a complimentary session with one of our advisers, you can click the button below or email us at customercare@gyc.com.sg.

Share

IMPORTANT NOTES: All rights reserved. The above article or post is strictly for information purposes and should not be construed as an offer or solicitation to deal in any product offered by GYC Financial Advisory. The above information or any portion thereof should not be reproduced, published, or used in any manner without the prior written consent of GYC. You may forward or share the link to the article or post to other persons using the share buttons above. Any projections, simulations or other forward-looking statements regarding future events or performance of the financial markets are not necessarily indicative of, and may differ from, actual events or results. Neither is past performance necessarily indicative of future performance. All forms of trading and investments carry risks, including losing your investment capital. You may wish to seek advice from a financial adviser before making a commitment to invest in any investment product. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product is suitable for you. Accordingly, neither GYC nor any of our directors, employees or Representatives can accept any liability whatsoever for any loss, whether direct or indirect, or consequential loss, that may arise from the use of information or opinions provided.