Should We Be Worried about the Market Sell-Off?

09 February 2018

While every investor acknowledges that there is risk when investing in the market, bouts of volatility and scary headlines still cause panic and make logic fly out of the window, triggering the ‘flight or fight’ mode for investors. We could spend hours discussing why the markets are down, what hedge funds and traders are doing, how central banks are adding to the woes, and still not come up with any satisfactory answer. The fact of the matter is this: nobody really knows why markets fell this week, and you really shouldn’t worry about the reason. Allow us to explain why.

Barely two weeks ago, market strategists and commentators were discussing the excellent start in January for stocks, which seems to bode well for the rest of the year. Everyone was trying to enthusiastically explain the reasons behind it: from rising interest rates to gently rising inflation. Fast forward that by one week and investors are left holding their heads in their hands, asking, “Why?” “Why did the Dow fall 4%? Why did the Hang Seng go down 5%? Why did the Nikkei go down 6%?” The very same commentators are now tripping over themselves desperately arguing that the markets were bound to fall because interest rates are rising and inflation is sure to jump as the economy heats up. This is surely adding to the confusion for many market watchers and investors!

Much has been written about how futile it is to try to predict short-term movements in market prices. But, if you have a good plan, have asset-allocated in line with your goals and risk tolerance, plus have time in the market, then you have good reasons not to worry about whether you had invested at the top or at the bottom of the market. Because in the long run, your portfolio will take care of itself, and give you the returns you need to achieve your goals. A stock market index like the Dow or S&P500 could lose 5% in a day, but a broadly-diversified portfolio holding both stocks and bonds could experience a drop of only 1 or 2%. The diversity of different country stocks, bonds and currencies within the portfolio will all act to spread out the risk and reduce the impact of such market blows. Keep your longer-term plan in perspective and don’t let such scary headlines cause you to lose sleep. Unless there is systemic risk building up, investors should not be fearful.

So when should we be more circumspect and be more careful? There are two situations which create a more longer-lasting and deeper market rout:

- Economic Recession

- Financial Crisis

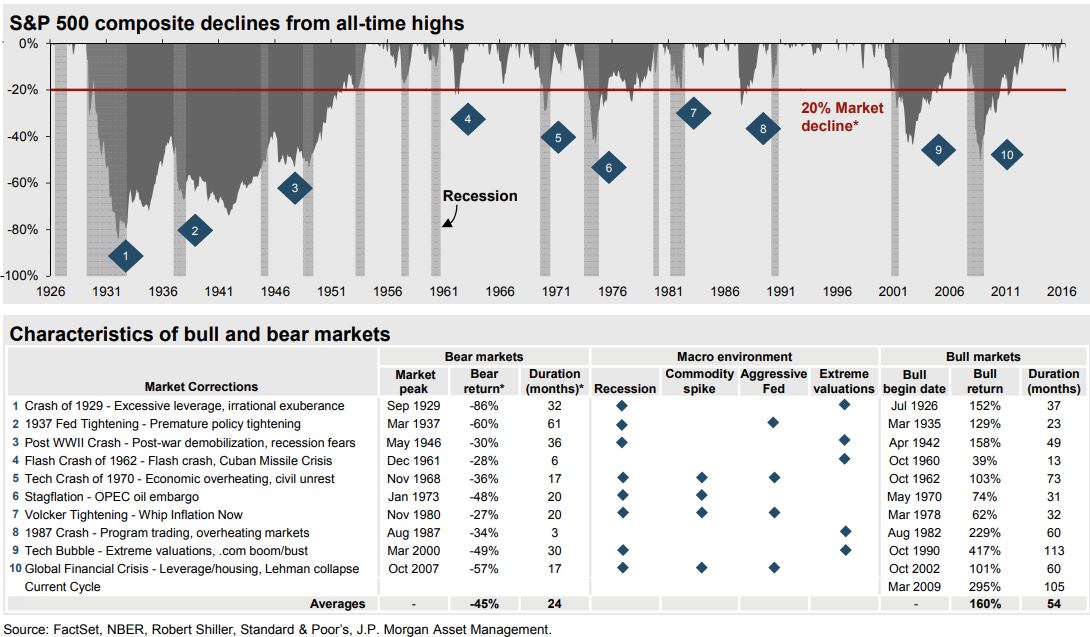

Bear markets created by either or both of these events are typically more long-drawn and have the capacity to greatly impair capital. The chart below shows the losses incurred and the duration of the bear market, with the exception of (4) and (8). These are the bear markets which we need to be more wary of. So the question we ask ourselves is whether there are currently any signals which indicate that a Recession or Financial Crisis is about to occur.

The following economic signals are part of the components and indicators which have been built into our proprietary Risk Matrix system. It helps us cut through the noise and confusing news flows to provide us with actionable insights into what is actually happening to the markets.

A. Signs of Economic Recession:

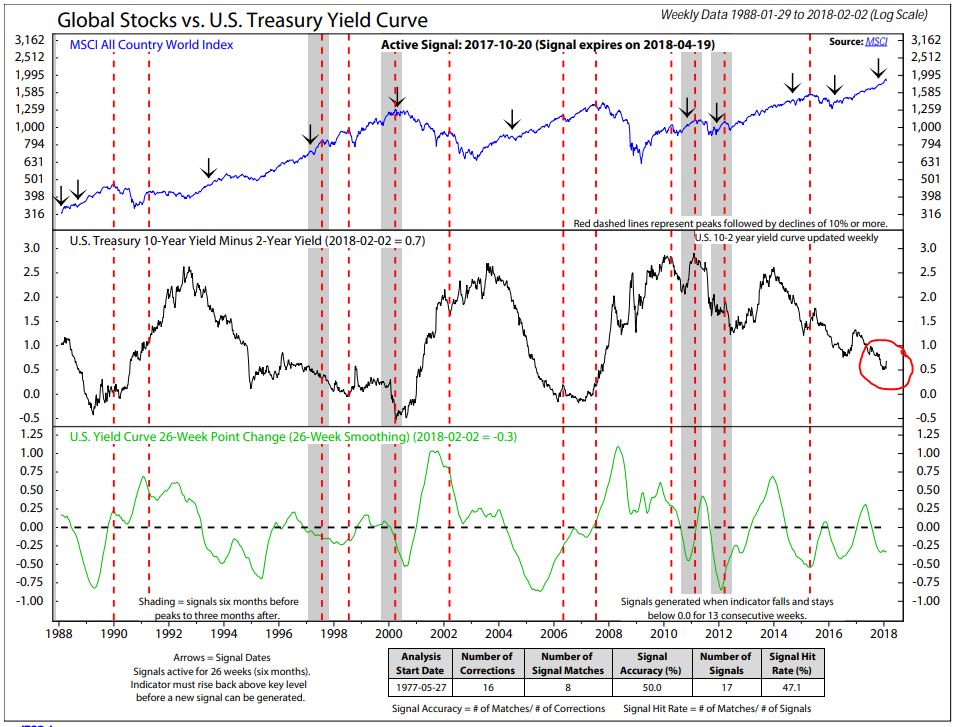

- Inverted Yield Curve: The chart below shows the current US yield curve (circled in red). Whilst it has decreased steadily over the past 4 years, it is nowhere as negative as in past market peaks of 2000 and 2007 (which preceded a deep recession).

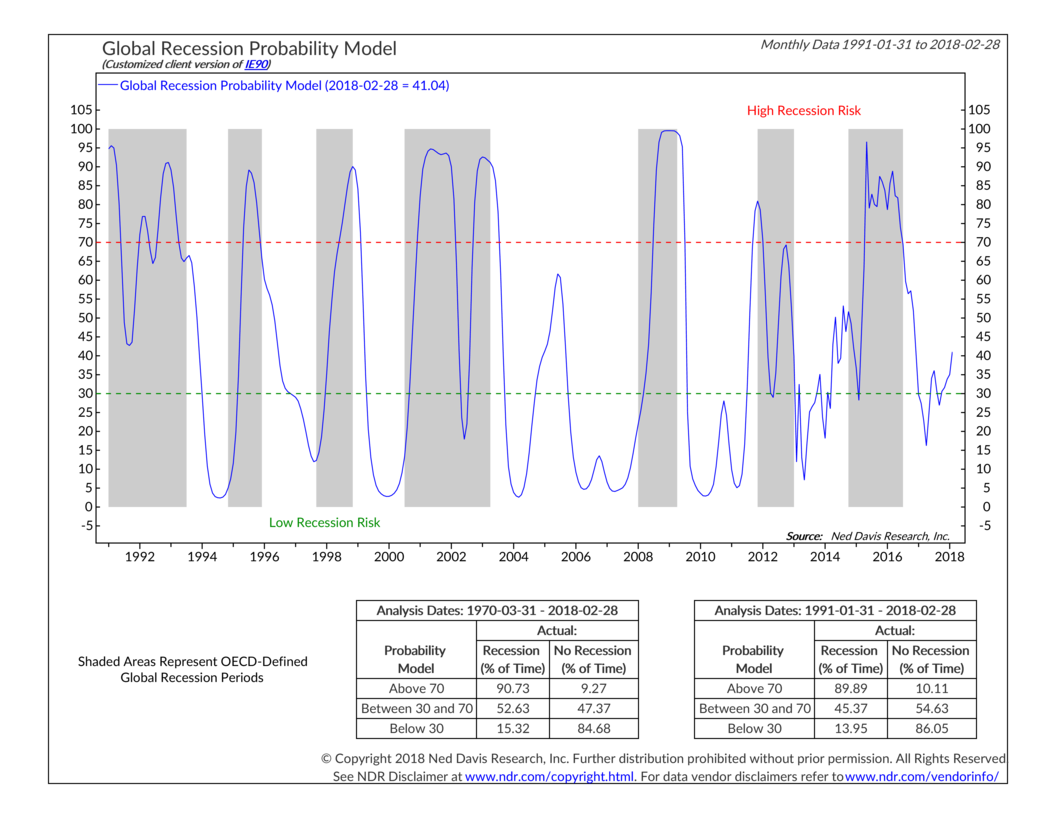

- Economic Leading Indicators: The chart below shows a composite of the OECD’s Composite Leading Indicators for 35 large economies around the world. The leading indicators consist of a wide range of economic indicators such as money supply, yield curve, building permits, consumer and business sentiment, share prices, and manufacturing production – all of which seek to give insights as to whether a country is doing well or not. At the moment, the indicator is signalling that a recession is not highly probable (see recession periods shaded in grey).

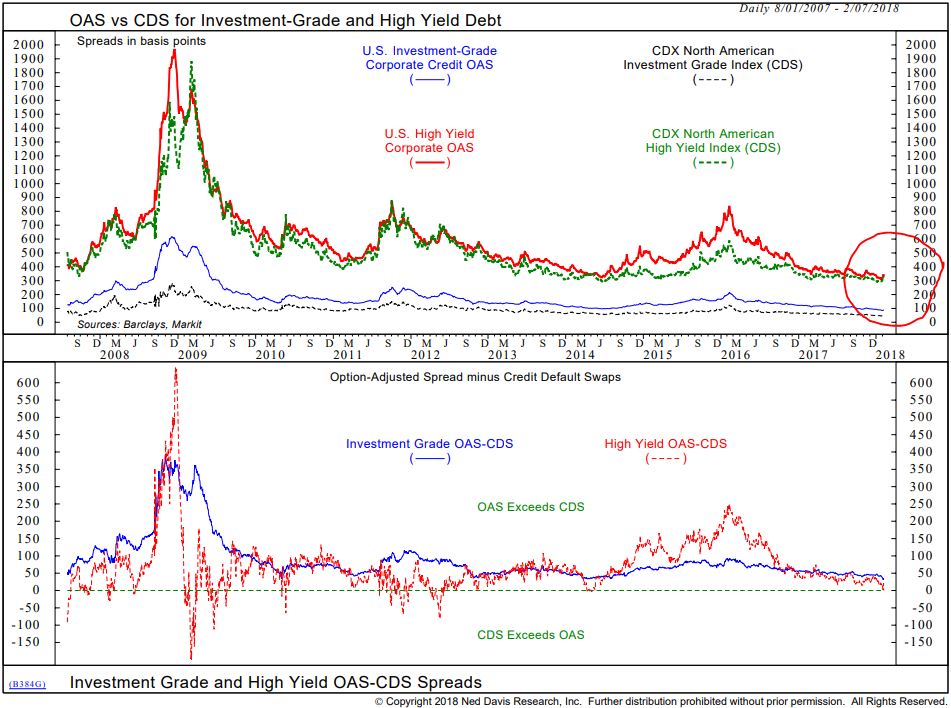

B. Signs of Financial Stress:

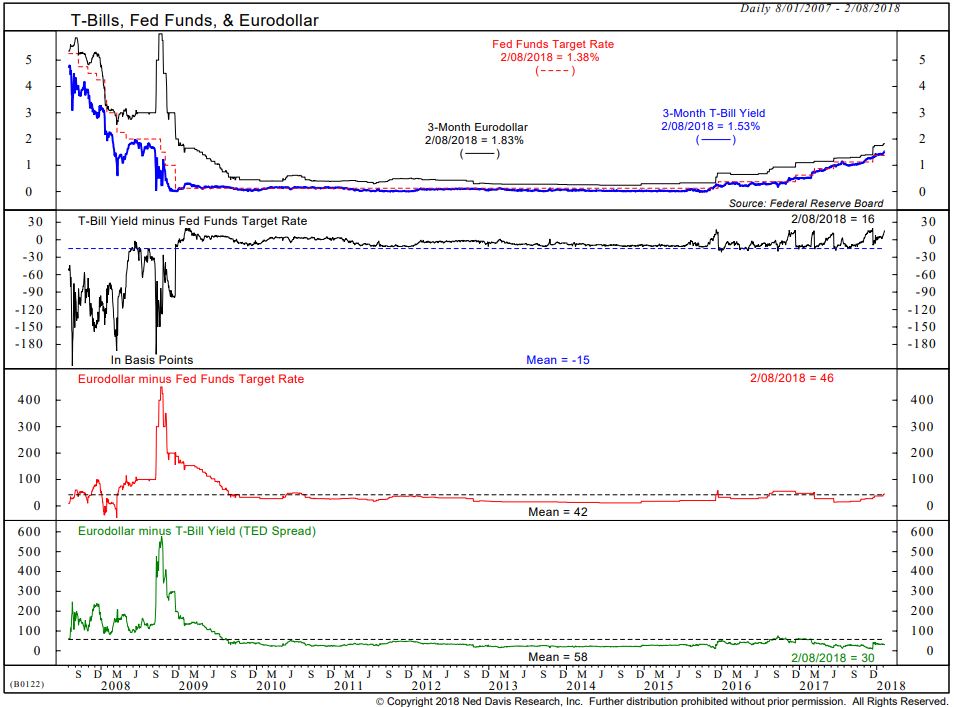

- LIBOR Spread: Despite talk of rising interest rates and the corresponding movement in bonds, a simple measure of financial stress in the system is whether financial institutions are lending to each other. During financial crises, when there is doubt over the ability of the counterparty to pay you back, lending rates typically spike and rise abruptly as there is no money supply available. The chart below shows current spreads to be still at very low levels (see comparison with the spikes reached during the Great Financial Crisis in 2008).

- Credit Spreads: During financial crises, when there are worries about the solvency of companies, the bonds that weaker companies (i.e. lower credit) issue typically get sold off. What happens is that you will then see the credit spreads increasing (i.e. the difference between the yield of an investment grade and low grade bond). Current credit spreads are near multi-year lows, showing that currently there is no sign of any financial stress (compare with the spikes reached in the 2008 GFC).

There are many more indicators that we track to confirm whether the market remains invest-able or not. But some of the major ones that we have shown above indicate that there is no sign of an impending recession nor financial crisis at the moment. What this ultimately means is that any sell-off in the markets is not likely to persist, nor will it be devastating to your portfolio. Markets still continue to function normally and you shouldn’t let such corrections derail you from your long-term goals. In fact, given the current signs, such corrections represent excellent opportunities to add more capital to investment portfolios as it means that assets are priced at a discount.

So what are the causes for the markets selling-off? It seems that as nobody knows for sure, let markets do what they are meant to do and focus on the other things that really matter in life. Stay the course, and don’t be fearful!

#

If you have found this article useful and would like to schedule a complimentary session with one of our advisers, you can click the button below or email us at customercare@gyc.com.sg.

Share

IMPORTANT NOTES: All rights reserved. The above article or post is strictly for information purposes and should not be construed as an offer or solicitation to deal in any product offered by GYC Financial Advisory. The above information or any portion thereof should not be reproduced, published, or used in any manner without the prior written consent of GYC. You may forward or share the link to the article or post to other persons using the share buttons above. Any projections, simulations or other forward-looking statements regarding future events or performance of the financial markets are not necessarily indicative of, and may differ from, actual events or results. Neither is past performance necessarily indicative of future performance. All forms of trading and investments carry risks, including losing your investment capital. You may wish to seek advice from a financial adviser before making a commitment to invest in any investment product. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product is suitable for you. Accordingly, neither GYC nor any of our directors, employees or Representatives can accept any liability whatsoever for any loss, whether direct or indirect, or consequential loss, that may arise from the use of information or opinions provided.