The Quirks of Concentrated Portfolios

10 August 2018

Imagine holding a slim portfolio of your favourite stocks – carefully curated from the chaos of the global market, specially selected for their reputation, performance, and potential to succeed. The idea can certainly be appealing. Many people feel safe when investing in companies and industries they are personally familiar with, especially if they have experiences – or connections – that could give them an edge.

“I know this company well,” they might say. “I’ve studied it for a long time.” Or, “I’m quite familiar with the business model of the firm.” Or even, “I have contacts who work there and know what’s happening in the industry.”

Sure, sometimes such investors get lucky and find themselves suddenly rolling in cash. But for many others, betting their entire portfolio on that small handful of stocks is an express train to financial ruin.

How many times have you bought a stock on sheer faith, only to see it tank and lose everything? Keppel Corp and Starhub used to be investors’ darlings, but who could have foreseen the sudden collapse in oil prices, or the sudden rise of Netflix and third party mobile providers?

Being a better investor starts with understanding that there are things you cannot control and things that you can. The ups and downs of the market – which directly affect a concentrated portfolio – fall into the first group. Being well-diversified falls into the second group.

Diversification – owning large groups of stocks, rather than just a handful – helps to spread your risk throughout the market and other countries, and thus reduces unforeseen or undesirable risks related to particular sectors or to individual securities. It also helps investors derive a more reliable level of return by smoothing out the ups and downs.

Many of you would be familiar with FAANG (Facebook, Amazon, Apple, Netflix, Google), an investing theme which has been dominating the markets these past few years. CNBC recently published an article describing how top-heavy the returns of these tech giants have been, even for this year. Investors who had focused on them would have been extremely happy.

However, when Facebook reported a revenue of $13B in their 26 July earnings report, at a 38% profit margin, shares inexplicably dropped over 20% and have been languishing around the same level since. Why did this happen? Logically, it made no sense. What made even less sense was that the entire tech sector was dragged down as a result, with a sudden outflow of money from assets tracking the tech sector.

But then, when Apple reported its earnings on 1 August, investors instead reacted favourably to the company, driving up its price until it became the first company to reach the $1 trillion market capitalisation level.

How do you explain the two very different investor reactions to two very similar events? Investors who had reacted to Facebook’s stock decline by selling out of the tech sector at a loss would have been left kicking themselves.

This is not a game that is easy to win. The rules are unpredictable and as arbitrary as luck and human nature. The better bet is not to make that bet at all on a specific stock or even a sector. Instead, just by owning the roughly 500 stocks in the US S&P 500 Index or the 2000-odd stocks from the global stock market, you would have received around an 8% and 4% return respectively, year-to-date in SGD terms. This would have given you much less hassle and heartache from the need to consider what to buy.

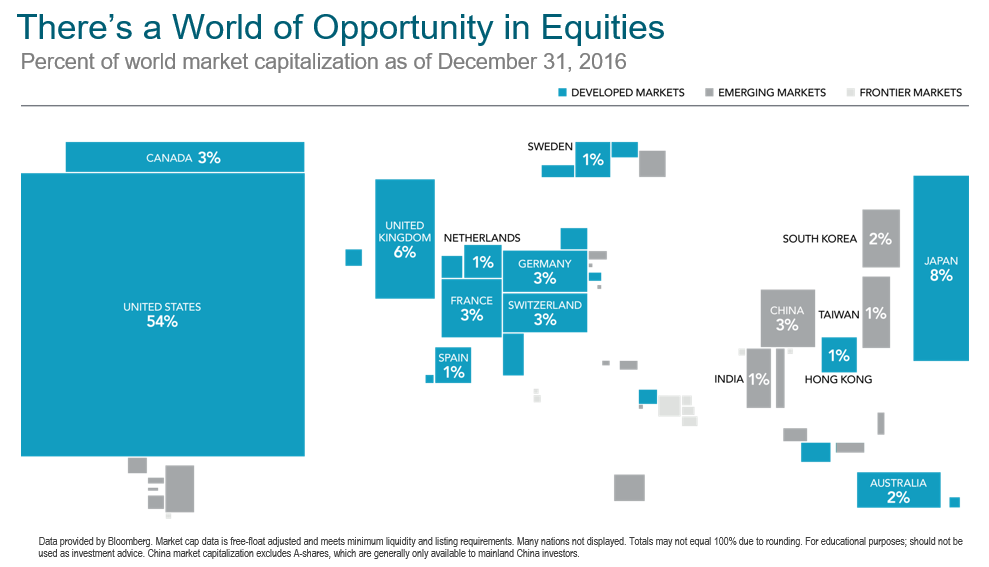

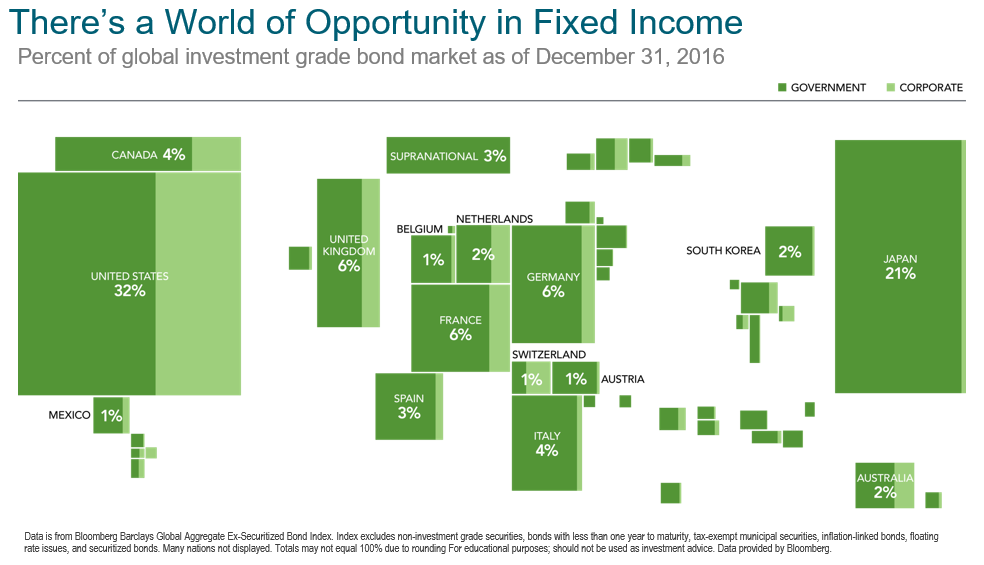

Diversification is not only about spreading risk between the tech sector, or banks, or property-related securities, or industrials. It’s also about having a diverse spread of investments across the world. The benefit of this is that whenever a particular stock, sector or country is out of favour, there will likely be others that will still be in favour and thus cancel out that loss, ensuring you continue to get a return, albeit a lower one – which is definitely preferable to a loss.

The graph below shows how much of each country’s listed assets form part of a globally-diversified portfolio. You may notice that Singapore is so small that it doesn’t even show up.

This also brings us back to some of the basic fundamentals of investing. Nobody can predict how prices are going to move, not even the ‘geniuses’ in Wall Street or (in our case) Raffles Place. We must also accept that prices always reflect all the available information from all investors’ expectations from around the world. Yes, prices may not be fair (and that is why asset bubbles occur), but prices are efficient and inherently impossible to forecast.

It is clear that it is hard to correctly and consistently anticipate what the best performing investment will be. That’s the bad news. The good news is, you don’t need to do it to have a reliable and positive investment experience.

Even when the whole world’s economy seems to be melting down (e.g. the 2008 Global Financial Crisis), there are investments which still hold their value well, like investment-grade government bonds and cash-like instruments. The key is not to panic and switch from one investment to another on a whim, but to ensure that you have a properly-constructed portfolio with a broad range of different asset classes. Understanding how the different asset classes like equity, fixed income, cash and even property work together is also important.

At the end of the day, if you are holding a properly diversified portfolio, the outcome of individual stocks or bonds don’t matter – and you can rest well, knowing that your investment journey will be a much smoother one.

#

If you have found this article useful and would like to schedule a complimentary session with one of our advisers, you can click the button below or email us at customercare@gyc.com.sg.

Share

IMPORTANT NOTES: All rights reserved. The above article or post is strictly for information purposes and should not be construed as an offer or solicitation to deal in any product offered by GYC Financial Advisory. The above information or any portion thereof should not be reproduced, published, or used in any manner without the prior written consent of GYC. You may forward or share the link to the article or post to other persons using the share buttons above. Any projections, simulations or other forward-looking statements regarding future events or performance of the financial markets are not necessarily indicative of, and may differ from, actual events or results. Neither is past performance necessarily indicative of future performance. All forms of trading and investments carry risks, including losing your investment capital. You may wish to seek advice from a financial adviser before making a commitment to invest in any investment product. In the event you choose not to seek advice from a financial adviser, you should consider whether the investment product is suitable for you. Accordingly, neither GYC nor any of our directors, employees or Representatives can accept any liability whatsoever for any loss, whether direct or indirect, or consequential loss, that may arise from the use of information or opinions provided.